WHERE’S THE EDGE III

What Is The Cantillon Effect?

The so-called Cantillon effect describes the uneven expansion of the amount of money. If a central bank pumps more money into the economy, the resulting increase in prices does not happen evenly. The Austrian economist Friedrich August von Hayek compared this monetary expansion with honey. If you pour honey into a cup, it won’t spread out evenly. It will clump in the middle of the cup first before spreading out.

Same with money: in case of a monetary expansion, the ones who profit from it are the ones who are close to the money. “Close to the money” in this case means everyone who can access the money right at the beginning, i.e. big companies, banks, etc. They get loans and make investments. Prices then start to rise even though the rest of the population has not received any of the new money yet. This part of the population usually is not the one with too much money. Nonetheless, they have to pay the higher prices even though they have not profited from the increase in money at all. And they will never profit from it in the same way as the ones who received the money first. The result is a redistribution from the poor to the rich.

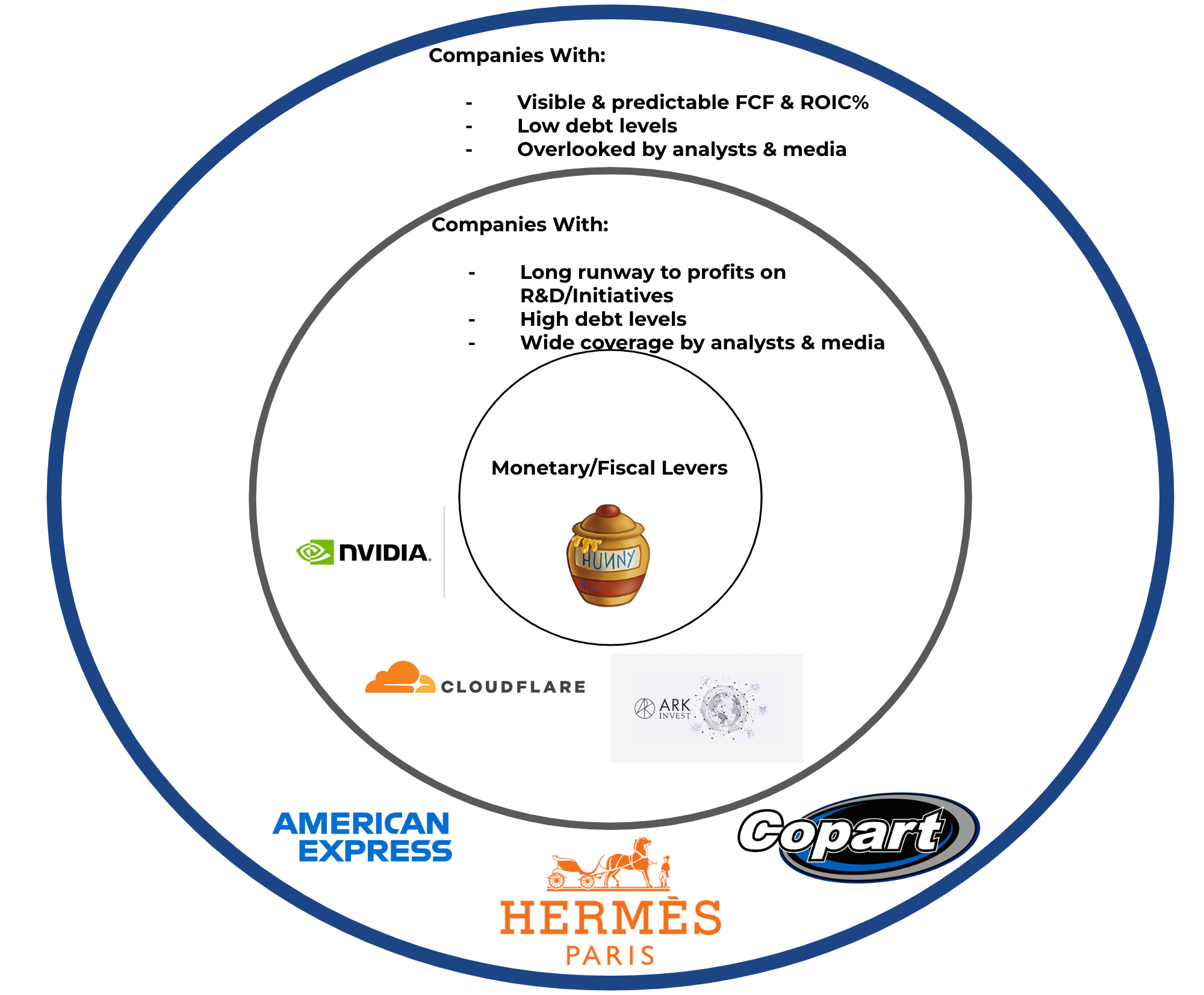

TLDR: Cantillon effect on assets is the sensitivity of businesses towards monetary and fiscal policies.

Businesses with a High Cantillon score tend to have the following attributes:

Longer than usual runway to profits (ie. Tech companies, Startups, etc)

High debt levels

Wide coverage by analysts & media

Businesses with a Low Cantillon score tend to have the following attributes:

Mature companies with visible & predictable Free-Cash-Flow

Low debt levels

Overlooked by analysts & media

When businesses possess 2 of 3 of the above attributes, we can more often than not definitively guess its sensitivity in relation to the ebb and flows of broader economic conditions. This concept of knowing business sensitivity is important because we want to build degrees of idiosyncrasies in our portfolio for an All-Terrain investment strategy. In addition, understanding the business sensitivity also helps identify where the key pools of capital are playing, from high- to low-time preference (recommended reading here). Playing in the high-time preference arena can be mentally exhausting because the churn of capital is high, and that translates to whip-saws on the tape, which can be destructive to an investor’s psyche; investments made in the high-time preference category should have a mental moat around the potential noise in the short-term (short-term to us refers to time frames of 3-9mths).

Fractal Nature Of Cantillon

Since the use of Cantillon here is an appropriation of concept to figuratively describe how businesses react to changes in the centre of gravity, be it economically or sectorial, it will be exemplary to indulge in a case study.

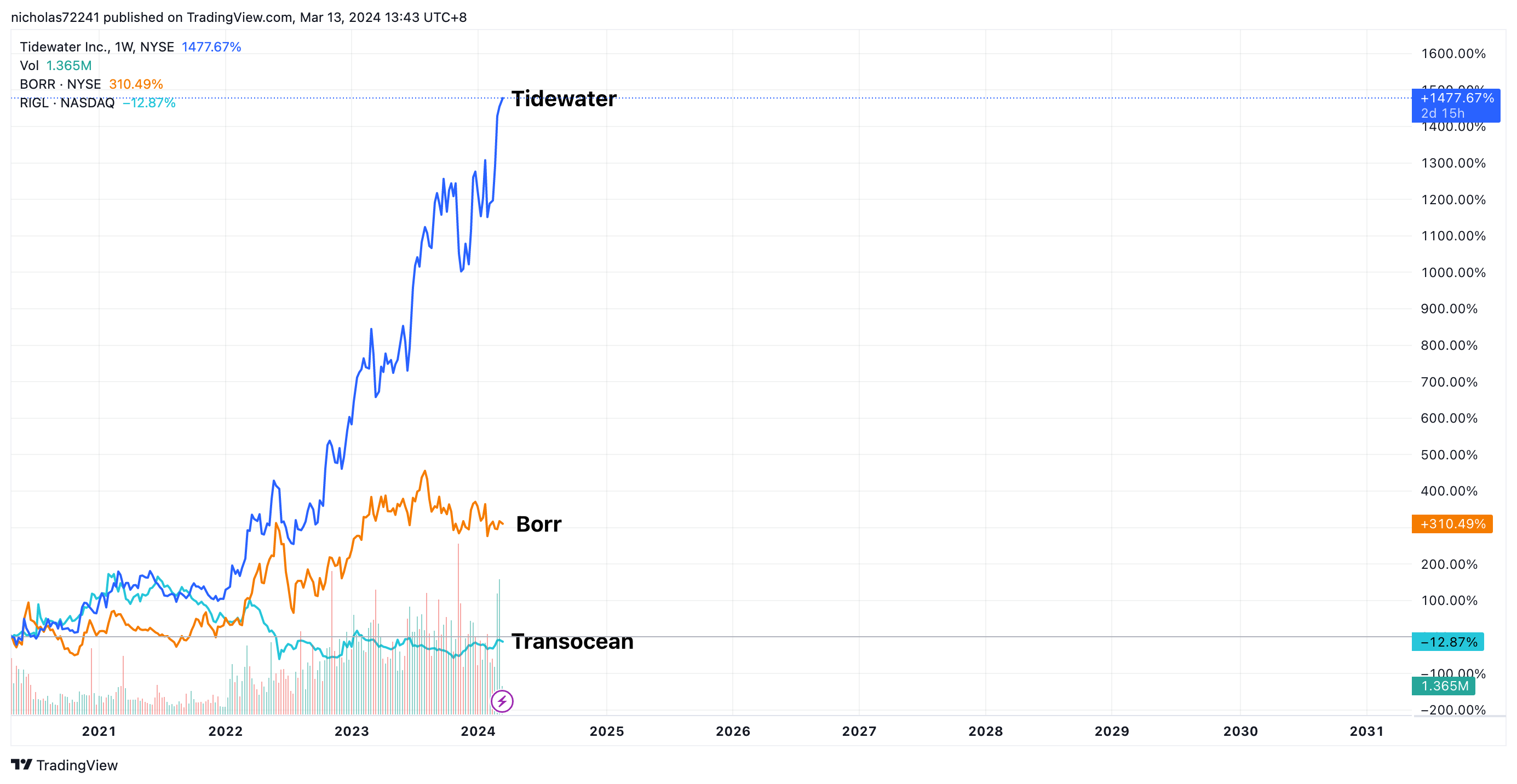

Offshore Oil Services is one sector that has been brutalised for many years since the peak of the previous cycle, and investors (stock investors & shipyards) are still suffering from the aftermath. The idea of the capital cycle suggests that at the bottom (max pessimism), cost discipline and consolidation amongst the survivors happen and this is when margins start to improve, and robust moats start to form if the barrier to entry for the industry remains high. These turnarounds usually happen under the radar at such points as beleaguered investors still remember the lingering trauma. This can be described as being far from Cantillion’s centre of gravity. Industries and companies far from Cantillon’s centre of gravity are akin to a long-dated far, out-of-the-money call option with no expiration date. Offshore is a long-cycle industry with many moving parts, namely segregated into Offshore Support Vessels (OSVs), Shallow-Water Drillships (Jackups) and Deep-Water to Ultra-Deepwater Drillships (DW, UDW). As you can imagine, Ultra-Deepwater vessels operates in the most demanding harshest conditions, requiring longer planning, more extended leasing and, hence, later-stage cycle winners. Now that the cycle offshore is starting to pick up again after ten years of value decimation, we can see the early-stage cycle beneficiaries like OSVs (NYSE: Tidewater) and Jackups (NYSE: BORR) starting to perform vs UDWs (NYSE: Transocean).

When pursuing asymmetric and robust absolute returns, a prudent investor may consider placing their bets on Borr and Transocean. The strategy involves anticipating the expansion of Offshore Cantillon's centre of gravity as the cycle progresses. This straightforward approach is often the path to discovering multi-baggers.

As can be seen above, when we juxtapose idiosyncratic industries like offshore against broad market names like NVIDIA, Ark Investment and Cloudflare, understanding sensitivity relative to the centres of gravity from the economic level down to the sectorial level can help one find the best risk-adjusted bet that will produce meaningful profits. This key point also helps reiterate the power of lagged effects and why real-alpha is always found "beyond the bend". It is so hard because it requires genuine faith and the byproduct of it, which is immense patience for just a probable chance of materializing, and most people just aren't wired to make this kind of money. But it is this kind of money that makes investing worthwhile because being able to "skate to where the puck is going" produces uncorrelated alpha (alpha that is not derived from closet indexing to S&500 or Nasdaq or whatever benchmark one runs against), and this is the kind of returns that is sustainable (buoyant in-spite of circumstance because the portfolio does not have to be entirely beholden to the ebbs and flow of the broad market) and has the potential for meaningful absolute returns if it's given a chance to compound over an extended period.

An important caveat is the fact that uncorrelated alpha cuts both ways. There will be periods when the portfolio will appear foolish relative to the broad market, producing neutral to even negative returns when all other indices are going up. Recognizing and resisting the urge to take corrective measures during such periods is what the best investors get paid to do, much more so than finding the next big thing. The Cantillon matrix is not so much a hard science of asset classification but rather a concept to approximate the timeline to asset performance based on the ebbs and flows of the global economy. This exercise in mental approximation helps fortify a reasonable mental moat to help investors resist the urge to act before Cantillon's time has yet to arrive.

“It never was my thinking that made the big money for me. It always was my sitting. Got that? My sitting tight! It is no trick at all to be right on the market. You always find lots of early bulls in bull markets and early bears in bear markets. I've known many men who were right at exactly the right time, and began buying or selling stocks when prices were at the very level which should show the greatest profit. And their experience invariably matched mine--that is, they made no real money out of it. Men who can both be right and sit tight are uncommon.”

―Edwin Lefèvre